The Share Market

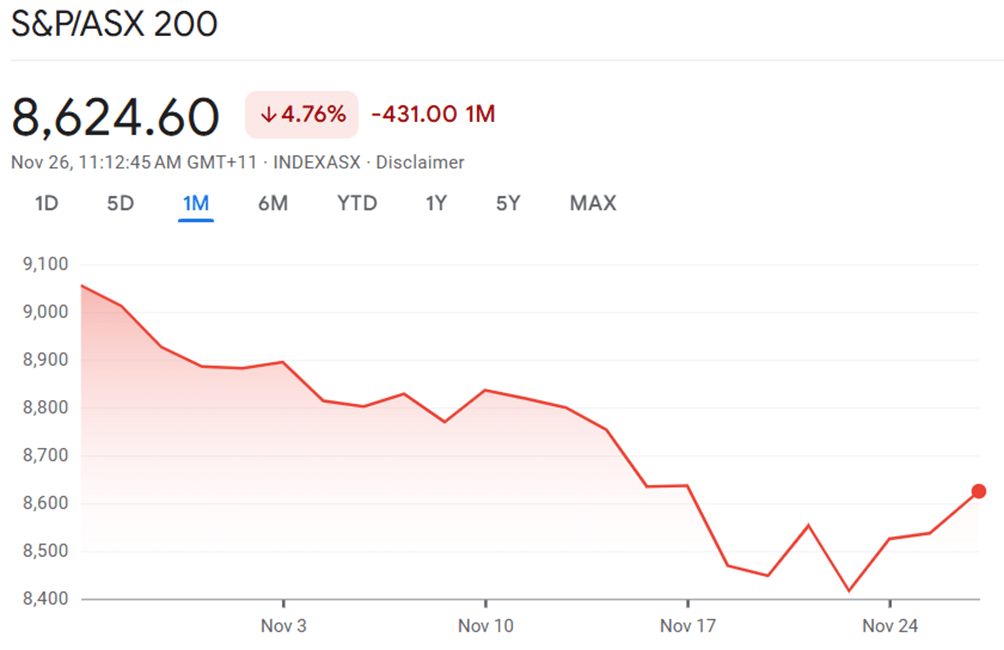

The S&P/ASX 200 has witnessed quite a turbulent ride through November 2025, according to data from Google Finance as at 26 November 2025. Meanwhile, the S&P 500 experienced a somewhat less severe downturn, as depicted in the second graph. This article explores the factors behind these major movements, and examines the interplay between the Australian and U.S. share markets over the month.

ASX 200 Performance

Throughout November, the S&P/ASX 200 index moved from above 9,000 points at the start of the month, only to fall to 8,624 by 26 November — a loss of 431 points, representing a drop of 4.76% for the month. The initial weeks saw a fairly consistent decline, with short-lived rallies failing to hold ground. The most significant fall occurred in the third week, pushing the index to a near six-month low before a modest recovery began in the last few days.

Source: Google Finance

Much of this volatility has been traced to several key events. Australian financial stocks faced significant downward pressure, with the sector dropping by more than 7% for the month, its worst showing since 2022. The major banks bore the brunt, affected by global uncertainty and upcoming interest rate decisions, which fuelled risk-off sentiment among investors. In contrast, mining stocks managed to advance at times, riding strong commodity prices and a rally in lithium and uranium shares, particularly following buoyant results from companies linked to the artificial intelligence boom in the U.S., such as NVIDIA.

Investor sentiment was also shaped by expectations about inflation. Approaching the end of November, traders anxiously awaited fresh monthly inflation figures, which were anticipated to show headline inflation climbing to 3.6%. The possibility of higher rates acted as a drag on valuations, especially in rate-sensitive segments like real estate and consumer discretionary.

Nevertheless, the market did stage a brief rally mid-month, buoyed by robust third-quarter earnings from U.S. tech giants and a recovery in global risk appetite. This lifted local tech stocks and provided a window for dip buyers in the financial sector to enter the fray, securing short-term rebounds. However, these gains proved fragile as the cautious mood returned, highlighted by a sharp sell-off and an eventual partial recovery after hitting the month's low on 21 November.

S&P 500 Performance

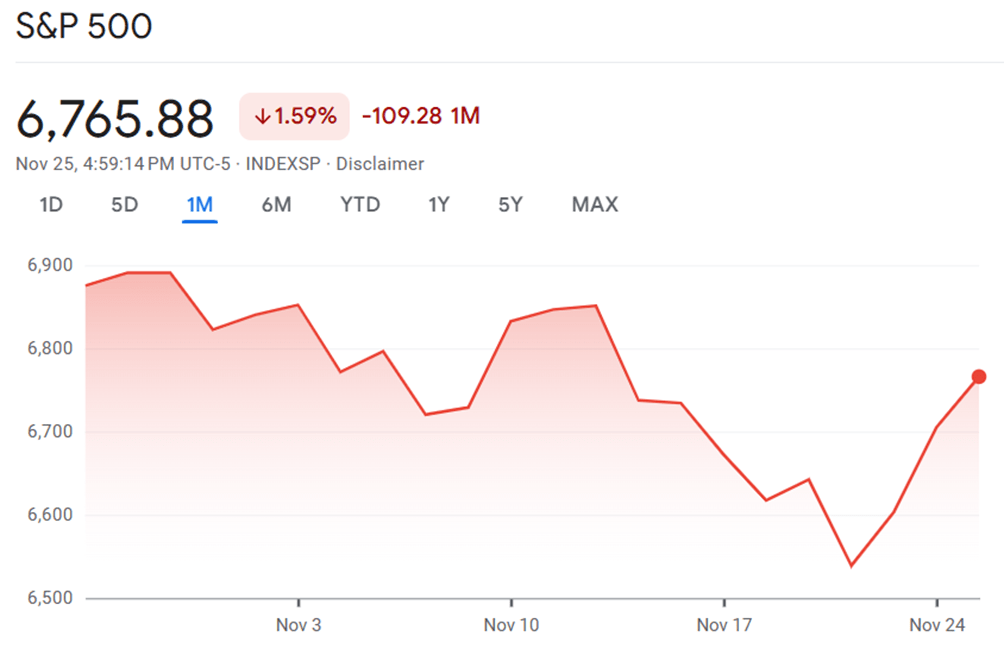

The S&P 500, for its part, charted a loss of 1.59%, falling from around 6,900 points at the beginning of November to 6,765 by 25 November. Like its Australian counterpart, it started the month on a strong note, only to see losses build in the second half, with the downward move led by technology stocks and heightened volatility around U.S. interest rate expectations.

Source: Google Finance

Major events behind these movements included investor concerns over stretched tech sector valuations ahead of crucial earnings releases, particularly for giants such as NVIDIA, Microsoft, and Amazon. These stocks faced sell-offs after mixed results and some disappointing forecasts, fuelling declines in the broader market. The so-called "Magnificent Seven" tech players were particularly impacted, whose volatility contributed to the market’s overall risk-off tone.

In addition, there was increasing speculation regarding possible rate cuts by the Federal Reserve, which stoked further uncertainty. Treasuries rallied as traders shifted into safer assets, while the dollar gained strength, making U.S. equities relatively less attractive for overseas investors. Nonetheless, the S&P 500 remained resilient, buoyed by select positive earnings in pharmaceuticals and gains in other defensive sectors. Late in the month, optimism returned on the back of expectations that rates would soon peak, helping drive a late rebound.

Comparing ASX 200 and S&P 500

While both indices declined during November, the ASX 200 posted a much steeper fall at 4.76%, over three times the percentage lost by the S&P 500 . Sector composition played a role — financial companies make up a much larger portion of the ASX 200 , and their outsized losses weighed heavily on the Australian market. Conversely, the S&P 500 benefits from greater sectoral diversification, with technology, healthcare, and consumer stocks providing more balance in times of volatility.

Currency factors further differentiate the response of the two markets. Australian shares are less exposed to currency risk for local investors, while those investing in the S&P 500 must contend with fluctuations in the U.S. dollar, which affected returns during a period of dollar strength.

Tax policy and dividend yields also frame the contrast. The ASX 200 is noted for its relatively higher dividend payouts and franking credits, which offer tax advantages to Australian shareholders—though these benefits were overshadowed by the sharp drop in bank shares this month. By comparison, the S&P 500 is driven more by capital growth, particularly among technology stocks, and typically offers lower income yields.

| Feature | ASX 200 | S&P 500 |

| % Change Nov 2025 | -4.76% | -1.59% |

| Key Hit Sectors | Financials | Technology |

| Late-month Rally | Modest, after deep sell-off | Stronger, tech-led |

| Sector Mix | Heavy financial/resources | Mixed, tech dominant |

| Major Risk Factor | Interest rates, inflation | Tech valuations, rates |

| Dividend Yield | Higher | Lower |

| Currency Risk | Minimal (for locals) | U.S. dollar exposure |

Conclusion

November 2025 proved tough for the ASX 200 , with financial stocks dragging the market lower, only partly offset by resource and tech rebounds. In contrast, the S&P 500 weathered volatility better, largely thanks to its tech and sector diversity, though it too felt pressure from shifting market sentiment and interest rate speculation. Both indices staged a rebound in the final week, but the ASX 200 ended the month worse off, highlighting the particular vulnerability of concentrated markets in times of economic uncertainty. International investors and local participants alike will be watching closely for signals of sustainable recovery in the months ahead.

The Residential Property Market

Australia’s residential property market remained in a strong upswing from October to November 2025, led by broad-based price gains and tight rental conditions. Growth is being driven by low stock, solid demand, and the new 5% Deposit Scheme, but affordability pressures are intensifying for many households.

Capital City Performance

National dwelling values rose 1.1% in October, the fastest monthly gain in more than two years, lifting annual growth to 6.1% and pushing the national median to about $872,500. Every capital city recorded a rise, with Perth, Brisbane and Darwin among the standout performers on both monthly and annual measures.

Key capital city indicators for October 2025 (dwellings):

| City | Monthly Change | Quarterly Change | Annual Change | Median Value |

| Perth | 1.9% | 5.4% | 9.4% | $884,471 |

| Brisbane | 1.8% | 4.9% | 10.8% | $992,864 |

| Darwin | 1.6% | 5.4% | 15.4% | $564,473 |

| Adelaide | 1.4% | 3.2% | 6.7% | $867,681 |

| Melbourne | 0.9% | 1.6% | 3.3% | $818,975 |

| Sydney | 0.7% | 2.3% | 4.0% | $1,256,156 |

| Canberra | 0.6% | 1.7% | 3.2% | $877,937 |

| Hobart | 0.3% | 0.5% | 2.4% | $686,262 |

Source: Cotality Home Value Index

Brisbane and Perth are benefiting from very tight listings and strong interstate and investor interest, while Darwin combines rapid value growth with the highest total returns due to strong rents and high yields. Sydney and Melbourne are still rising but at a slower pace, reflecting stretched affordability and more cautious buyer sentiment in the larger, more expensive markets.

What is Driving the Upswing?

The key engine of this phase is a pronounced supply–demand imbalance. Estimated home sales are running about 3% above the five‑year average, while advertised listings are roughly 18% below average, meaning more buyers are competing for fewer homes. On the construction side, dwelling commencements and completions remain well below decade averages, and higher building costs and industry insolvencies are limiting the pipeline of new supply.

Earlier interest rate cuts in 2025 boosted borrowing capacity and helped turn prices around, but the Reserve Bank paused in November and economists now see little chance of further cuts before 2026. With borrowing power gains largely offset by the price increases since February, further growth will rely more on population, incomes, lending policy and ongoing tight supply than on cheaper credit.

The 5% Deposit Scheme

On 1 October 2025, the federal government converted and expanded its earlier guarantee programs into the Australian Government 5% Deposit Scheme. Under the new settings, eligible first‑home buyers can purchase with as little as a 5% deposit (and some single parents with 2%), with no lenders mortgage insurance, uncapped places, and higher property price caps, subject to location limits.

Early data show a sharp uplift in take‑up. Government figures indicate nearly 5,800 first‑home buyer guarantees were issued in October, about 50% higher than a year earlier before the expansion. This demand is feeding directly into the lower and middle price segments: across the combined capitals, October value growth was strongest in the middle (up 1.4%) and lower quartiles (up 1.2%), compared with 0.7% for the upper quartile.

The scheme effectively lowers the deposit hurdle and can bring forward purchases for households who might otherwise spend years saving, especially in cities where a 20% deposit now takes more than a decade to accumulate. However, because it boosts demand in a market where supply is already constrained, the scheme also risks adding to price pressures in entry‑level segments unless it is matched by policies that expand new housing supply.

Rental Market and Yields

Record‑low vacancy rates of around 1.4% have pushed rents higher again, with the national rental index rising about 0.5% per month in recent months. Smaller capitals such as Darwin and Hobart have led annual rental growth, while unit rents are outpacing houses in most cities as tenants look for more affordable options and inner‑city stock is absorbed.

Despite solid rental growth, prices have been rising even faster, so gross yields have edged down to about 3.4% in the capitals and 4.3% in regional areas, the lowest since 2022. Investor interest remains firm in high‑yield markets such as Darwin and parts of regional Western Australia and Queensland, although regulators are increasingly alert to the rapid growth in investor credit.

Affordability and Outlook

Rapid price gains since 2020 mean home values are now around half again higher than pre‑pandemic levels in many areas, pushing ownership further out of reach for households without parental support or access to schemes. Affordability stress, high living costs and a softer labour market are emerging as key brakes that could moderate growth even if supply stays tight.

Most forecasters expect price growth to continue into 2026, but at a slower and more uneven pace as stretched affordability and policy risks, such as possible tighter investor lending standards, start to bite. For now, the October–November 2025 period marks one of the strongest phases of the current cycle, with markets like Perth, Brisbane and many regional hubs still gaining ground, while Sydney and Melbourne step more cautiously under the weight of high prices and buyer fatigue.

Inflation and Interest Rates

As November 2025 draws to a close, Australian households find themselves in a familiar position: waiting. On 4 November, the Reserve Bank of Australia (RBA) Board decided to keep the official cash rate on hold at 3.60%.

For many, this was a tough pill to swallow. Hopes had been high for a pre-Christmas rate cut to ease the pressure on mortgages. However, the data simply didn't support it. The RBA has made it clear that while we are past the peak of the crisis, the job isn't quite finished.

The primary reason for this pause is inflation’s stubborn refusal to drop further. The September quarter Consumer Price Index (CPI) revealed headline inflation had risen to 3.2%, up from 2.1% in the previous quarter.

More importantly, the trimmed mean inflation, the RBA’s preferred gauge of underlying price pressure, remains at 3.0%. This sits right at the very top of the RBA’s target band. Governor Michele Bullock noted that while goods inflation has eased, "service inflation" (costs related to things like healthcare, education, and insurance) remains high due to wage growth and steady demand.

The Forecast Shift

This unexpected stickiness in prices has forced major economists to rewrite their timelines. Earlier in the year, optimism for late 2025 cuts was high, but that has now evaporated.

- Westpac and NAB have pushed back their forecasts for the next rate cut, now looking towards May 2026.

- Commonwealth Bank has adopted an even more cautious stance, predicting no further cuts in the immediate term as the RBA waits for service inflation to crack.

The Consensus: The economy is in a bind. With underlying inflation stuck at 3.0%, the RBA cannot cut rates; yet with unemployment drifting up to 4.5%, the economy is too fragile to hike them. We are effectively stuck in a holding pattern.

What This Means for Your Wallet

- Mortgages: If you are on a variable rate, your repayments will remain steady for now. The relief many hoped for is likely delayed until next year.

- Savings: For those with cash in the bank, this is good news. With the cash rate holding at 3.60%, interest rates on savings accounts and term deposits remain attractive.

- Daily Costs: While prices aren't skyrocketing as they did in 2022, they are still creeping up. The 3.2% inflation figure means your money is losing value slightly faster than it was a few months ago.

Looking Ahead

The road to economic normality is proving longer than anticipated. While we have avoided a recession, securing low and stable inflation is taking time. For now, patience is the watchword as we look towards 2026 for the next shift in monetary policy.