The Share Market

March 2026 was the kind of month that makes investors uneasy. Markets didn’t just drift lower — they moved sharply, often unpredictably, and always with a sense that something bigger was unfolding in the background.

Looking at the ASX 200 and the US S&P 500, the overall direction is clear: both fell over the month. But the way they got there — and the reasons behind those moves — tell a more interesting story.

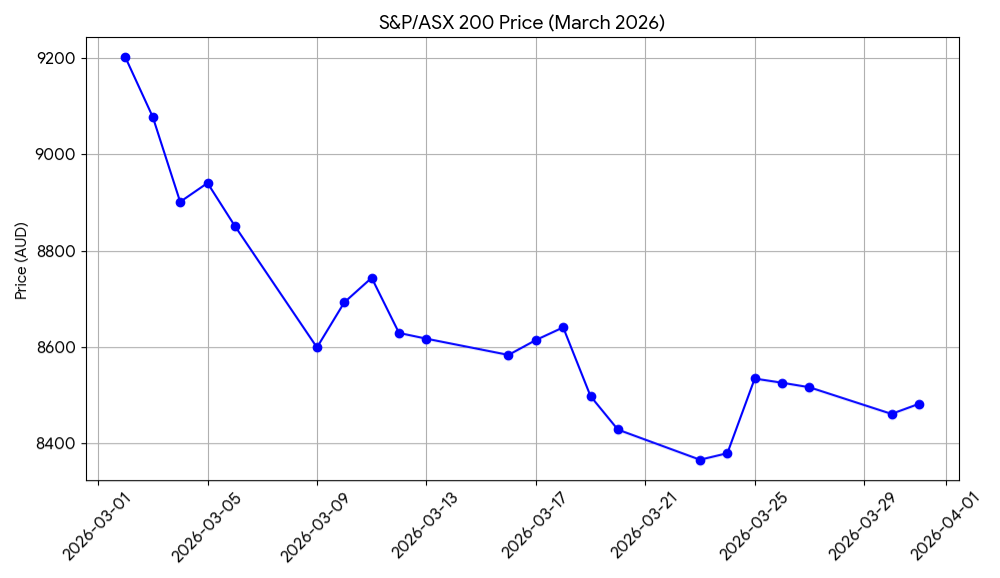

ASX 200

Source: Based on Data from Google Finance

In Australia, the month began from a position of strength. The ASX 200 was sitting near record highs, around the 9200 mark, and there was little immediate sign of trouble. That changed quickly.

Within the first week, the market dropped sharply. It wasn’t a slow loss of confidence, it was a sudden shift. From there, the pattern became more drawn out: brief recoveries followed by continued weakness, eventually pushing the index down into the mid-8300s before a modest rebound at the end of the month.

What caused that shift wasn’t something happening on Collins Street or in Canberra. It was global.

Tensions in the Middle East escalated significantly during March, particularly involving the United States and Iran. For markets, the most immediate concern wasn’t the conflict itself, but what it meant for energy supply. Oil prices surged as traders priced in the risk of disruption to key shipping routes.

That matters more than it might seem at first glance. When oil prices rise quickly, the effects ripple through the economy — petrol becomes more expensive, transport costs increase, and businesses start facing higher input costs. All of that feeds into inflation.

And inflation, in turn, puts central banks in a difficult position.

Large institutions, including J.P. Morgan, highlighted this shift toward a more fragmented and unstable global backdrop in their March outlook.

For Australian households, the implications were fairly direct. If inflation stays higher for longer, interest rates are more likely to remain elevated, or even rise further. That affects mortgage repayments, discretionary spending, and overall confidence.

There were already signs that sentiment was weakening. A Westpac consumer confidence report released mid-month showed that while the headline number held up slightly, responses later in the survey period became noticeably more pessimistic, reflecting growing concern about the economic outlook.

That shift in mood matters because markets don’t just reflect current conditions — they reflect expectations. If households and businesses start to pull back, investors tend to react early.

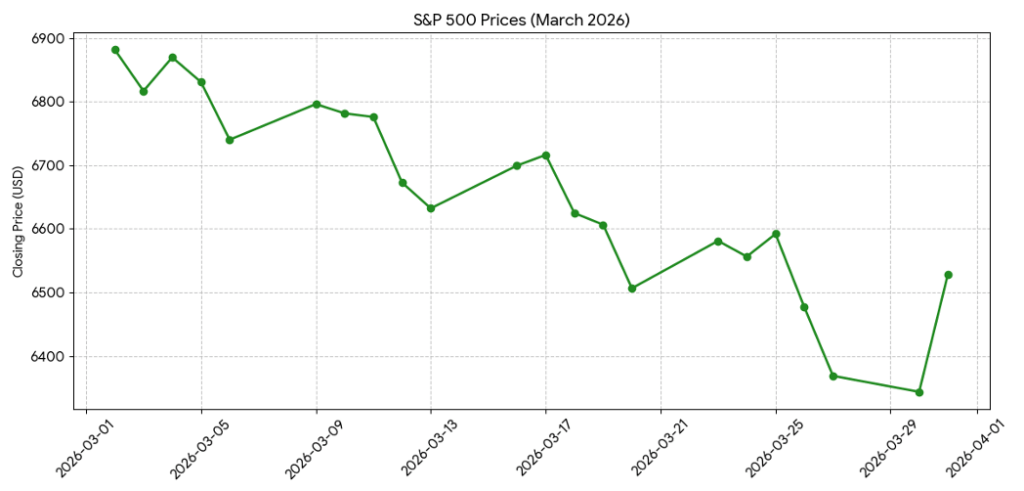

S&P 500

Source: Based on Data from Google Finance

While the Australian market declined in a relatively steady way, the United States told a more volatile story.

The S&P 500 also trended downward across March, but the path was far less smooth. Instead of a gradual slide, the index moved in sharp bursts — falling, rebounding, and then falling again. By the final week of the month, it reached its lowest point before staging a noticeable bounce right at the end.

This more erratic pattern comes down, in part, to what the US market is made of. The S&P 500 is heavily weighted toward large technology and growth companies — businesses whose valuations are particularly sensitive to interest rates and inflation.

When oil prices spike and inflation fears pick up, investors start reassessing those valuations. Higher interest rates reduce the appeal of future earnings, which can put pressure on growth stocks. At the same time, uncertainty around global supply chains and economic growth adds another layer of caution.

The result is a market that reacts quickly, and sometimes sharply, to new information.

Comparing the Two Markets

One interesting difference between the two markets is how they responded to rising energy prices.

Australia’s market, while still falling overall, has a meaningful exposure to mining and energy companies. When commodity prices rise, those sectors can benefit, providing some support to the broader index.

The US market doesn’t have that same cushion to the same extent. As a result, it was more exposed to the negative side of the inflation story, particularly later in the month, when concerns appeared to peak.

Conclusion

It’s important, though, not to oversimplify what happened.

The Middle East conflict and the surge in oil prices were clearly major drivers. But markets were also responding to a mix of other factors, including:

- expectations around interest rates in both Australia and the US

- shifting investor positioning after a strong start to the year

- broader concerns about global economic growth

In reality, markets rarely move for just one reason. March was a good example of how multiple pressures can build at once, creating the kind of volatility that feels sudden, even when it has been developing beneath the surface.

Looking back, the month serves as a reminder of how quickly global events can filter through to everyday investors.

You don’t need to follow every geopolitical headline to feel the impact. If you have superannuation, investments, or even just a mortgage, shifts in inflation, interest rates, and global confidence can reach you fairly quickly.

That’s what March 2026 showed not just that markets can fall, but how interconnected the world’s financial systems have become, and how events far from Australia can still shape outcomes at home.

The Residential Property Market

It has been a highly eventful first quarter for the Australian property sector. Here is a look at how the market performed throughout March 2026 and what we might expect as we head further into the year. The information below is drawn directly from the Cotality Home Value Index report for April 2026, alongside reputable insights from established market analysts.

A Diverging Market in March

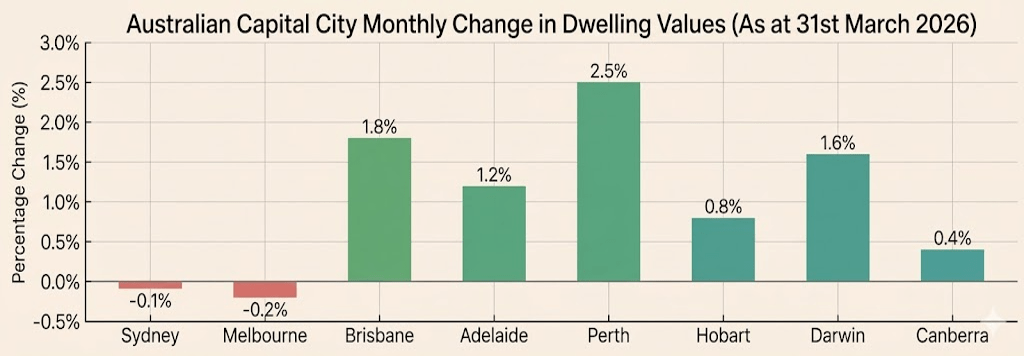

As we closed out the first quarter of 2026, the national home value index rose by 0.7% in March. This took national dwelling values 2.1% higher over the first three months of the year. However, the headline figure masks an increasingly diverse set of outcomes from city to city.

At one end of the spectrum, our largest capital cities are experiencing a subtle decline. Since the end of November 2025, values in Melbourne have retreated by 0.9%, while the Sydney market is down by 0.4%. This softer trend coincides with falling auction clearance rates and a noticeable increase in advertised supply, which is providing buyers in these cities with more choice and far less urgency at the negotiation table.

Conversely, the mid-sized capitals, along with Darwin, are continuing to break records, recording month-on-month growth of 1.2% or more. Perth remains the standout performer, accelerating in the face of higher interest rates. Housing values across the western capital jumped by 2.5% in March, sitting 7.3% higher over the quarter.

Below is a snapshot of how the major markets performed up to the end of March 2026, based on a synthesis of Cotality and broader market data:

Sources: Cotality HVI April 2026

A Shift in Momentum

The "two-speed" nature of the Australian property sector has never been more apparent. While Sydney and Melbourne cool, buyer demand is heavily concentrated in more affordable regions.

Conditions are also splintering across broad value tiers, with lower-priced homes clearly leading the pace of growth. This trend is most noticeable in Sydney, where upper-quartile dwelling values fell by 1.8% through the March quarter, while the lower quartile actually increased by 1.8%. Tighter borrowing limits are pushing buyer demand towards the more affordable end of the market, where they are competing with first-home buyers and heightened investor activity.

Beyond the capital cities, regional markets are demonstrating impressive hardiness to the broader slowdown. Regional Western Australia is a prime example, with areas like Bunbury seeing values jump 8.4% through the March quarter to sit 22.2% higher over the past 12 months.

The Rental Crunch

For tenants across the country, the situation remains incredibly challenging. National vacancy rates hovered around a staggering 1.1% in early March, with cities like Perth, Adelaide, and Brisbane experiencing even tighter conditions.

According to reports from AAP News, rents grew by 5.7% over the past 12 months. With vacancy rates sitting near record lows, there is significant upward pressure on asking rents, offering no immediate relief for those trying to secure a lease this year.

Why Prices Keep Rising

It is entirely valid to wonder why property values in places like Perth and Brisbane continue to surge despite consecutive Reserve Bank of Australia (RBA) rate hikes, which pushed the cash rate to 4.10% in March.

The primary driver remains a chronic undersupply of housing. In Perth, the number of homes advertised for sale is roughly 40% below the five-year average. When inventory is this tight, even dampened buyer demand is enough to force prices upward. Additionally, the rising cost of construction materials (partly fuelled by global energy shocks and oil prices surpassing US$119 a barrel) means the pipeline of new housing supply remains severely restricted.

What’s Next?

The recent cash rate hikes have undoubtedly eroded borrowing power, and broader cost-of-living pressures are weighing heavily on consumer confidence. However, Australia's low unemployment rate and strong labour market continue to act as a stabiliser, preventing forced sales.

Despite the rapid growth in certain pockets, there are early signs that overall purchasing demand is beginning to ease. Recent estimates show that quarterly home sales are tracking 1.9% lower than a year ago and remain 5.6% below the five-year average. Consumer confidence has weakened materially as cost-of-living pressures and international geopolitical uncertainties intensify. Given the likelihood of these pressures persisting, experts anticipate that purchasing demand will continue to soften over the coming months.

This gradual shift toward more balanced market conditions is expected to support a further, albeit uneven, slowdown in housing value growth throughout the remainder of 2026. The ongoing balance between stretched affordability, tight supply, and the potential for further economic shocks will be the central theme to watch.

Inflation and Interest Rates

As we move through the first quarter of 2026, many Australians are feeling a familiar squeeze on their household budgets. After a period of relative stability in 2025, the start of this year has brought a renewed sense of caution to our domestic economy. I recently spoke with a small business owner in Melbourne who noted that while customer numbers remain steady, the average spend has noticeably dipped as people tighten their belts in response to the latest headlines.

The economic data from March reflects this shift, showing a complex interplay between global events and local price pressures.

The Return of Interest Rate Hikes

In a move that surprised some market observers but followed weeks of growing speculation, the Reserve Bank of Australia (RBA) raised the official cash rate in March. At its meeting on 17 March, the Board decided to increase the cash rate target by 25 basis points to 4.10%.

This decision marks a significant turn in policy. Throughout much of late 2025, the RBA had held rates steady, and there was even talk of potential cuts. However, the Board noted that "inflationary pressures picked up materially in the second half of 2025" and that the risks have now "tilted further to the upside."

Inflationary Pressures and the CPI

The latest figures from the Australian Bureau of Statistics (ABS) provide the backdrop for the RBA's hawkish stance. The monthly Consumer Price Index (CPI) indicator rose 3.7% in the 12 months to February 2026. While this was a slight easing from the 3.8% recorded in January, it remains stubbornly above the RBA’s target range of 2–3%.

Housing continues to be the primary driver of inflation, with costs in this sector rising by 7.2%. This includes significant increases in rents and electricity prices, the latter being impacted by the expiration of previous government rebates. In addition, recent global tensions in the Middle East have pushed automotive fuel prices higher, a factor that is expected to filter through to the March and April data.

Looking Ahead

The outlook for the remainder of 2026 remains uncertain. Deloitte Access Economics has warned that the Australian economy is "running on empty," with growth expected to slow to 1.9% for the 2026-27 financial year. While unemployment remains low by historical standards, the combination of higher borrowing costs and persistent price rises for essentials like food and fuel is expected to weigh heavily on consumer confidence. For Australian families, the March rate hike means an immediate focus on mortgage repayments and discretionary spending. As the RBA continues to monitor global energy prices and domestic demand, the path back to the 2–3% inflation target appears longer than many had hoped at the start of the year.